BIMTECH Business Perspectives

Search

Search

Sonali Sonali1, Shabir Hussain2 , Sameer Gupta1 and Sunil Bhardwaj2

, Sameer Gupta1 and Sunil Bhardwaj2

1The Business School, University of Jammu, Jammu and Kashmir, India

2School of Management Studies, University of Jammu, Bhaderwah, Doda, Jammu and Kashmir, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Purpose: This study introduces an integrated conceptual framework elucidating the interconnections between excessive use of social networking sites (SNSs), financial shock (FS), and digital financial services usage behaviour (DFSUB) in relation to individual financial well-being (FWB). Furthermore, it examines the roles of financial knowledge (FK) and financial inclusion (FI) as mediating mechanisms within these relationships.

Design/methodology: The manuscript employs a scoping review of peer-reviewed literature concerning FWB and its antecedents. It utilises the information–motivation–behavioural skills (IMB) model to organise existing evidence and to develop six propositions that link excessive use of SNSs, FS, DFSUB, FK, FI and FWB.

Findings: The proposed framework posits that excessive engagement with SNSs and FS is negatively related to FWB. Conversely, the behaviour associated with the use of digital financial services (DFS) is positively related to FWB. Furthermore, the framework advances the propositions that FK serves as a mediator in the relationship between excessive use of SNSs and FWB, and that FI mediates the relationships between FS, DFSUB and FWB.

Practical implications: The conceptual model illustrates that policymakers and practitioners have the capacity to formulate strategies that enhance financial literacy, increase inclusive access to formal financial services and foster the responsible and effective use of DFS. These strategies aim to equip individuals with the necessary skills to navigate the impacts of social media and financial disruptions, ultimately contributing to improved FWB.

Originality/value: This study expands the IMB model into the realm of FWB by conceptualising excessive SNSs usage, FS, DFS usage, FK and FI as an integrated framework. It further articulates theoretically grounded propositions that can be empirically tested in future research across diverse populations and contexts.

Financial well-being, financial shock, social networking sites, digital financial service usage behaviour, financial knowledge, financial inclusion

Introduction

With the global increase in poverty and inequality (Bashir & Qureshi, 2023), financial well-being (FWB) has emerged as a key topic of interest (Brüggen et al., 2017; Riitsalu et al., 2024). FWB is described as a facet of well-being that includes feelings of financial satisfaction and security (Vlaev & Elliott, 2014). Regardless of one’s level of interest in financial issues, FWB is essential in our lives, both presently and in the future. Attaining FWB enables individuals to concentrate on their financial objectives, alleviate ongoing financial stress and look forward to a prosperous future (García-Mata et al., 2022; García-Mata & Zerón-Félix, 2022). This underscores the importance of achieving and sustaining FWB for individuals and families, as it affects their overall well-being by providing a foundation for fulfilling basic needs, pursuing personal financial goals and managing unforeseen expenses or emergencies (Dare et al., 2023; Fatma et al., 2022; Kumar et al., 2023). Furthermore, Vlaev and Elliott (2014) suggest that FWB is not solely reliant on the amount of money one has, but rather on the ability to manage financial resources effectively. As a result, FWB is considered a vital link to several key Sustainable Development Goals (Fu, 2020).

Moreover, due to technological advancements, the financial sector has transformed from traditional banking to customer-centric digital solutions, including digital financial services (DFS) (Hussain et al., 2025b). This shift is exemplified by the emergence of fintech, which is revolutionising the way consumers manage payments, savings, investments and bank accounts (Zhang & Fan, 2024). DFS refers to a group of diverse financial services that can be accessed and delivered through various digital channels (Hussain et al., 2025a). It has the potential to increase financial inclusion (FI) by giving marginalised people more inexpensive, quick and secure access to financial services (Hasan et al., 2022), and leading to positive FWB (Bhatia & Dawar, 2023).

Furthermore, the significant growth of digitalisation has enabled individuals to become more socially active via the internet, which offers a multitude of ways to access and share information (Fu et al., 2020). Social networking services (SNSs) are widely utilised today (Fioravanti et al., 2021), providing people with digital platforms for interaction and information collection (She et al., 2023). However, excessive SNSs usage encourages spending through users’ extravagant lifestyles and targeted marketing while adversely affecting behaviours such as online shopping, credit misuse, materialism and conspicuous consumption, consequently impacting FWB (Chatterjee et al., 2019; She et al., 2021; Wilcox & Stephen, 2013). Nevertheless, if an SNSs user possesses financial knowledge (FK), materialistic tendencies can be reduced (Gutter & Copur, 2011).

Likewise, in an increasingly volatile global economy, unforeseen financial shocks (FS) such as sudden income loss or unexpected large expenditures represent a major external threat that can rapidly undermine individuals’ financial stability and overall well-being (Bufe et al., 2022). However, if a person is financially included, then they can have access to various banking services such as insurance services, savings, borrowing and investing, which provides safety, security and transaction transparency and may build financial stability, which will increase their well-being (Belayeth Hussain et al., 2019; Kass-Hanna et al., 2022).

This study is important as researchers contend that achieving FWB requires easy access to suitable financial services and the FK to achieve financial objectives, highlighting the important role of FK and FI (Riitsalu & Murakas, 2019). Therefore, on the basis of an extensive review of FWB literature, our study fills the gap on how SNSs, DFSUB and FS impact FWB, with FK and FI acting as mediators between excessive use of SNSs and FWB and between FS, and DFS usage behaviour and FWB using the information–motivation–behavioural (IMB) skill model, which has not been widely utilised in FWB studies. Consequently, this research proposes an integrated conceptual framework for FWB, incorporating FK and FI as mediators between excessive SNSs usage and FWB, DFSUB, FS and FWB. In addressing this research issue, the study raises the following questions:

This study aims to offer readers and marketers a fresh perspective on FWB and encourage them to explore new ideas by understanding the impact of excessive SNSs usage, FS and DFSUB on FWB and the mediating role of FK and FI between excessive use of SNSs and FWB and between FS, DFSUB and FWB using the IMB model of an individual. The significant outcome of this study is the proposition of a conceptual framework that paves the way for researchers in the future to test the model and reach generalisable results empirically. This study adopts a scoping review of the literature approach in identifying the gaps in the research continuum. On the basis of the reviewed literature, an integrated conceptual framework is developed based on the propositions posited in this study. Hence, assisting the policymakers and practitioners in devising strategies to increase FK and FI to improve FWB.

The structure of the article is as follows. We start with an introduction where we define the concept of FWB and outline the research issues. Following this, the second section details the research methodology. The review of literature and propositions are presented in the third section. In the fourth section, we introduce our proposed conceptual framework. The fifth and sixth sections cover the implications and conclusion, respectively. The final section addresses the limitations and offers suggestions for future research.

Research Methodology

This research undertook an exploratory investigation by examining a broad spectrum of academic literature concerning FWB and its precursors, drawing on previously published works from academic journals, magazines and periodicals. The objectives of this study necessitated a descriptive research approach. It predominantly uses secondary data. The aim was to pinpoint various determinants of FWB and to investigate the mediating influence of FK and FI on the connection between excessive use of SNSs and FWB, as well as between FS, DFSUB and FWB.

This study reviews existing literature and utilises a well-established methodology introduced by Jabareen (2009) to elucidate the review process. This method has been instrumental in developing theoretical frameworks across various interdisciplinary research (Basu et al., 2019; Gupta et al., 2024; Ringelstein & Patel, 2023), making it a suitable option. The methodology comprises several phases that are tailored to align with the specific requirements of the current study. The distinct methodological phases are delineated as follows:

Phase 1: Data Collection

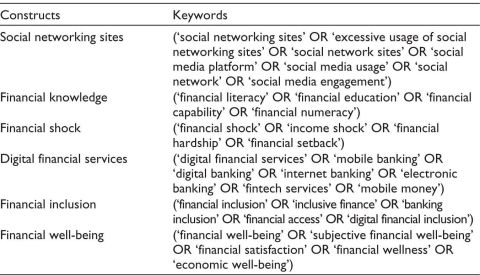

The data collection process began with identifying and retrieving literature relevant to FWB. A structured keyword search strategy was used, with similar terms mentioned in Table 1. These combinations ensured comprehensive coverage of FWB constructs. The search was conducted in leading databases, including Scopus, Web of Science and Google Scholar.

Table 1. Structured Keywords to Search Relevant Literature.

The articles were identified through initial research from Scopus, Web of Science and Google Scholar. Following title, abstract screening, duplicate removal and full-text eligibility assessment for theoretical relevance to FWB antecedents, articles published between 2014 and 2025 were selected to construct the conceptual framework and six propositions. This timeframe was selected to capture the strong, escalating trend in FWB research since 2014 (Kaur et al., 2021).

Phase 2: Screening and Shortlisting

Once data were collected from the selected databases, several reading sessions were organised to refine the selection process. Initially, the titles and abstracts of all extracted articles were screened to assess their alignment with the research objectives. To ensure quality, only peer-reviewed articles published in journals indexed in Scopus and listed in the Australian Business Deans Council (ABDC) were considered for further evaluation. The full texts of these selected articles were then carefully analysed to determine their theoretical and methodological compatibility with research questions and objectives. Ultimately, 27 studies were included, which significantly contributed to the development of the conceptual framework and six propositions.

Phase 3: Analysis and Synthesis

The shortlisted articles were then analysed based on the research objectives. The authors here adopted a deductive approach to conduct the review. As a result, the review attributed to the synthesis of the proposed conceptual framework based on how each construct influences or contributes to FWB.

Phase 4: Reporting of Review Outcomes

The final step was to report the results in different sections based on the study’s research objectives.

Review of Literature and Propositions

Information–Motivational–Behavioural Skill (IMB) Model

The IMB model, initially developed by Fisher and Fisher to forecast health behaviour, has been proven effective in predicting and altering various behaviours (Fisher, 1992). This model consists of three fundamental elements: information, motivation and behavioural skills. ‘Information’ encompasses facts, heuristics and implicit theories, while ‘motivation’ includes both personal and social aspects. In contrast, ‘behavioural skills’ refer to the abilities and self-efficacy required to apply these skills in different contexts (Fisher, 1992). This model has been used to predict a number of behaviours, including HIV medication adherence, voting behaviour, financial behaviour, recycling behaviour, use of smokeless tobacco (Amico et al., 2009; Glasford, 2008; Limbu, 2017; Seacat & Northrup, 2010; Shell et al., 2011). In this study, to understand how individuals achieve and maintain FWB amid digitalisation and financial uncertainty, the IMB model is employed as its primary theoretical framework. Where SNSs and FK are regarded as sources of information (Lusardi, 2012; Teo et al., 2019; Tsai & Men, 2017). However, excessive use of SNSs can lead to impulsive consumption behaviours in individuals (She et al., 2021; Thoumrungroje, 2018). Conversely, FK offers pertinent information that can mitigate the negative effects (specifically associated with the overuse of SNSs) (Santini et al., 2019).

Furthermore, FS and FI act as motivational forces. While FS is an external occurrence, it serves as a catalyst that spurs individuals to pursue financial security by taking protective measures such as saving, purchasing insurance and utilising formal financial services (Bufe et al., 2022; Kulshreshtha et al., 2023). Meanwhile, FI encourages individuals to utilise all banking services available to address uncertainties (Bhatia & Dawar, 2023; Nandru et al., 2021). Moreover, in the context of the IMB framework, DFSUB is identified as a behavioural-skill competency (i.e., practical skills) essential for the effective use of DFS to improve FWB (Kumar et al., 2023; Rahman et al., 2020; Zhang & Fan, 2024). Additionally, FI offers the motivational and structural resources (such as institutional access and affordability) needed to transform these skills into better financial outcomes (Yang & Zhang, 2022). Based on the IMB model, this research introduces a conceptual framework that includes excessive use of SNSs, FS, DFSUB and FWB. It suggests that FK acts as a mediator in the link between excessive SNSs usage and FWB, while FI serves as a mediator in the relationship connecting FS, DFSUB and FWB.

FWB

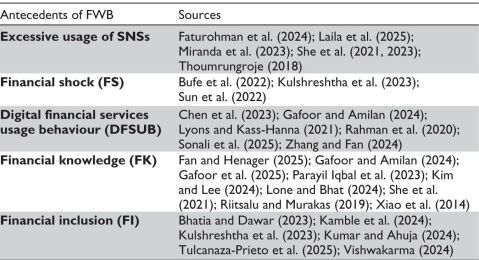

In light of contemporary global economic challenges and uncertainties, FWB has assumed increased importance across all stages of life. Research characterises FWB as an individual’s confidence in their financial circumstances, encompassing their capacity to pay bills, fulfil financial obligations and maintain surplus funds for both current and future needs (Salignac et al., 2020). An individual’s ability to meet financial responsibilities, both presently and in the future, alongside their perception of financial independence, constitutes their FWB (Mahendru et al., 2022). This concept is bifurcated into two components: the stress associated with managing current finances and the anticipation of future financial security (Netemeyer et al., 2018). Importantly, the impact of FWB extends beyond economic factors, influencing overall health and mental well-being (Shim et al., 2009). Brüggen et al. (2017) delineate three categories of FWB definitions or measures: (a) those combining objective and subjective methods, (b) those employing solely objective methods and (c) those utilising solely subjective methods. The first category describes FWB as a composite concept that affects financial assessment (Shim et al., 2009). The second category utilises various financial condition indicators, such as financial ratios (Greninger et al., 1996) and objective financial status (Hira & Mugenda, 1998), to evaluate FWB, whereas the third focuses on subjective financial satisfaction (Xiao et al., 2014). The current emphasis on financial stability underscores the complexity of FWB, which involves achieving goals, managing the present, preparing for the future, and fully enjoying life. This interconnectedness underscores the profound effects of financial health on both economic and overall life (Netemeyer et al., 2018; Shim et al., 2009). In this study, Table 2 represents the reviewed literature on the antecedents of FWB.

Table 2. Reviewed Literature on the Antecedents of FWB.

Excessive Usage of SNSs and FWB

SNSs are now commonplace communication tools used by people, businesses and organisations to boost online social interaction (Fu et al., 2020). These platforms foster a lively setting for the spread and reception of information by offering multiple methods to access and distribute content, while also providing users with entertainment, opportunities for social engagement and means for retrieving information (Teo et al., 2019; Tsai & Men, 2017). These benefits ensure its popularity among users and significantly influence their lives and behaviours (Ketelaar et al., 2016; Liu et al., 2019; Shang et al., 2017). In recent years, scholars have increasingly raised concerns about the addictive nature of SNSs usage, particularly among young working adults who are allocating more time to these platforms and frequently depending on them as their primary source of information (Dwivedi & Lewis, 2021; Grau et al., 2019).

Research has shown that excessive use of SNSs can have negative consequences for users (Faturohman et al., 2024; Miranda et al., 2023). Studies by Thoumrungroje (2018), Kelly et al. (2018), Thorisdottir et al. (2019) and She et al. (2023) emphasise the harmful effects of excessive use of SNSs on personal well-being, including encouraging materialism, leading to overspending, promoting credit misuse and increasing conspicuous consumption. Consequently, our study proposes a negative relationship between excessive SNSs usage and FWB.

Proposition 1: There is a negative relationship between the excessive usage of SNSs and FWB.

FK Mediates the Relationship Between Excessive Usage of SNSs and FWB

FK denotes ‘the understanding of fundamental financial investment principles such as inflation and risk diversification, along with the ability to perform calculations related to interest rates’ (Lusardi, 2012). Enhanced FK contributes to anticipated future financial stability and alleviates current financial management stress (Netemeyer et al., 2018). Research indicates that FK enhances financial behaviour, such as reducing credit card misuse and materialism, which positively affects FWB and financial satisfaction (Fan & Henager, 2025; Gafoor et al., 2025; Gutter & Copur, 2011; Xiao et al., 2014). Individuals with higher levels of financial literacy demonstrate a heightened ability to detect financial fraud and exhibit a greater propensity to seek professional financial advice or counselling compared to those with lower literacy levels, ultimately enhancing their FWB and mitigating adverse repayment scenarios (Engels et al., 2021; Hwang & Park, 2023). Consequently, our study posits that FK serves as a mediator in the relationship between excessive SNSs usage and FWB.

Proposition 2: FK mediates the relationship between excessive SNSs usage and FWB.

FS and FWB

FS can arise from a decrease in income, such as losing a job or having reduced work hours, or from increased expenses, such as costly repairs, medical emergencies or legal fees related to divorce or other matters (Bufe et al., 2022). These unforeseen events present external challenges to individuals or families, necessitating adjustments and causing stress, which influences the overall financial health and underscores the importance of resilience and adaptive strategies in overcoming these challenges (Bufe et al., 2022; Kulshreshtha et al., 2023; Sun et al., 2022). Therefore, our study suggests a negative relationship between FS and FWB.

Proposition 3: There is a negative relationship between FS and FWB.

DFSUB and FWB

DFS includes a diverse range of services offered and accessed via digital platforms, such as credit, payments, savings and insurance (Nizam & Rashidi, 2025). These services are facilitated by a range of devices, including electronic cards, chips, tablets, phablets, biometric devices and other electronic systems (Hasan et al., 2022; Rana et al., 2020). While technology assists users by removing geographical and temporal limitations and enhancing convenience (Yang & Zhang, 2022). The previous literature suggests that DFS usage behaviour positively influences FWB (Chen et al., 2023; French et al., 2020; Rahman et al., 2020; Sonali et al., 2025). Consequently, this study posits a positive relationship between DFSUB and FWB.

Proposition 4: There is a positive relationship between DFSUB and FWB.

FI Mediates the Relationship Between FS and FWB

FI involves the effort to provide financial education, access, availability, affordability and the use of essential financial services to underprivileged groups in society, particularly focusing on marginalised street vendors, to improve their FWB (Nandru et al., 2021). As Mpofu and Mhlanga (2022) and Nandru et al. (2021) point out, the expansion of mobile money banking services has been crucial in providing financial access to millions of previously unreached individuals. This makes financial transactions more accessible, trustworthy and safe. According to Bhatia and Dawar (2023) and Vishwakarma (2024), a FI strategy helps people deal with FS and improves their overall FWB. In conclusion, FI is critical because it increases access to financial services while also building financial stability. This enables people to better manage financial setbacks and enhances their overall FWB. Consequently, this study proposes a mediating role of FI between FS and FWB.

Proposition 5: FI mediates the relationship between FS and FWB.

FI Mediates the Relationship Between DFSUB and FWB

FI involves the effort to provide financial education, access, availability, affordability and use of essential financial services to underprivileged groups in society to improve their FWB (Nandru et al., 2021). Buckley and Malady (2009) highlight the crucial role of DFS as an essential financial solution in promoting FI to achieve comprehensive FWB (Gafoor & Amilan, 2024; Nandru et al., 2021). DFS leverages digital technology to enhance the financial landscape for various stakeholders, increasing access and serving as a key tool to bolster FI (Yang & Zhang, 2022). This illustrates the transformative impact of DFS in addressing the challenges of FI and paving the way for enhanced FWB for individuals and businesses. Therefore, our study suggests that FI mediates the relationship between DFSUB and FWB scores.

Proposition 6: FI mediates the relationship between DFSUB and FWB.

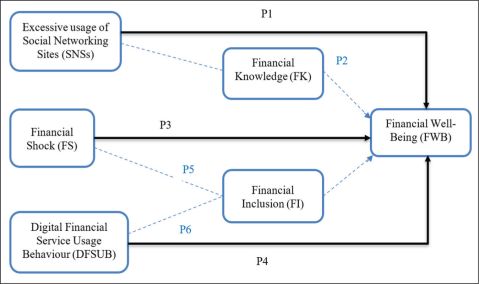

Proposed Conceptual Framework

The present study has identified several informational, motivational and behavioural-skill factors that potentially influence individuals’ FWB. The informational factors include excessive use of SNSs and FK. While SNSs create a dynamic environment for exchanging information, excessive use of these platforms exposes individuals to impulsive, materialistic cues that may negatively affect their FWB. Nevertheless, adequate FK can equip individuals to make informed financial decisions and thereby influence their FWB positively. Thus, based on the existing literature, it is expected that excessive use of SNSs negatively impacts FWB, whereas FK positively mediates the relationship between excessive SNSs usage and FWB. Furthermore, the motivational factors include FS and FI. When individuals experience sudden losses such as income disruptions, health emergencies or property damage, these shocks negatively affect their FWB; however, such experiences and FI motivate them to avail financial protection through insurance, savings and retirement products offered by the financial sector. Accordingly, FI is expected to positively mediate the relationship between FS and FWB. In addition, DFSUB represents the behavioural-skill factor, referring to individuals’ ability to confidently use DFS, such as mobile banking for managing their finances effectively, which in turn enhances their FWB as mobile banking reduces financial inequalities in accessing financial services (such as insurance, savings and budgeting) without time and physical constraints. Thus, these accessibilities improve the FWB of an individual. Hence, it is expected that DFSUB positively impacts FWB and FI positively mediates the relationship between DFSUB and FWB. These informational, motivational and behavioural-skill factors are conceptualised as potential antecedents of the FWB construct, expected to exert a significant influence on individuals’ FWB.

As mentioned in the previous section, the propositions from Proposition 1 to Proposition 6 reflect this core ideation. Accordingly, the proposed conceptual framework has been developed to depict the relationships among these factors as antecedents of individuals’ FWB (Figure 1).

Figure 1. Conceptual Framework.

Source: Authors’ own conceptualisation by compiling IMB skill model and the relevant existing literature.

Implications of the Study

The proposed conceptual framework outlines several clear implications by systematically aligning each proposition with the IMB model:

Theoretical Contribution

The model expands the IMB model in the domain of FWB by explicitly linking excessive use of SNSs and FK to the information component, FS and FI to motivational aspects and DFSUB to behavioural skills. This systematic arrangement clarifies how informational, motivational and skill-based elements collectively shape financial outcomes in a digital environment, offering a fresh perspective on how to recover from shock in the digital age.

Second, the study proposes that FK acts as an intermediary between excessive SNSs usage and FWB, while FI serves as a mediator between both FS and DFSUB and FWB. This establishes specific pathways through which digital and shock-related experiences influence financial outcomes. This approach goes beyond direct-effect models by emphasising how knowledge and access serve as protective mechanisms that can mitigate or direct the effects of risky informational environments (excessive SNSs usage) and adverse events (FS). These mediating roles encourage future theoretical development on when and how informational and institutional resources transform potentially harmful exposures into adaptive financial behaviours.

Third, the framework reimagines the precursors of FWB as an interconnected system rather than as separate factors: excessive SNSs usage is viewed as a harmful informational setting which can have a negative impact on FWB, FS as a destabilising motivational catalyst impacts FWB negatively, DFS usage as a skill enhances FWB, and FI acts as a supportive structural context. This holistic perspective implies that FWB theories should consider digital behaviours, shock exposure and institutional access simultaneously, rather than treating them as distinct elements. It also creates opportunities for cross-cultural and longitudinal exploration of how shifts in digital ecosystems, inclusion policies and household shocks alter the equilibrium among information, motivation and behavioural skills over time.

Policy Implication

This study provides various implications for policymakers. For policymakers, this involves developing targeted programmes to enhance financial literacy by leveraging peer-to-peer networks to facilitate knowledge transfer from those with expertise to those with less understanding. This also includes improving access to inclusive financial systems and ensuring that DFS are both secure and affordable. Additionally, policymakers can identify and empower ‘local champions’—such as leaders in cooperatives, Anganwadi workers, members of self-help groups, small business owners and school teachers—to provide focused financial education on topics like saving, investing, budgeting, retirement planning and accessing banking services through both online and offline platforms, thereby building resilience against uncertainties. These champions should also educate communities about the pitfalls of excessive use of SNSs like impulsive buying and materialistic behaviour, encouraging informed decision-making to enhance FWB.

Managerial Implications

This research offers practical guidance for financial advisers, emphasising that excessive use of SNSs and FS can adversely affect FWB. Based on these findings, financial advisers/planners can suggest several strategies to their clients. First, they should recommend setting up a monthly budget to track income against both fixed and variable costs. Second, automating savings transfers to cover 3–6 months of emergency expenses is advisable. Third, reducing time spent on social media can help lessen materialistic influences and control impulsive spending. Fourth, clients can benefit from free apps or online courses that teach budgeting and investment basics to improve their FK. Financial advisers can identify customers with gaps in FK and tailor sessions to teach practical skills, such as using budgeting apps and distinguishing between needs and wants influenced by SNSs.

Conclusion

This article introduces a detailed conceptual framework grounded in the IMB model to elucidate how digitalisation and FS collectively influence FWB. The primary theoretical contribution is the expansion of the IMB model into the FWB domain by identifying specific mediating pathways through which DFSUB and FS impact FWB. Specifically, FK mediates the relationship between excessive SNSs usage and FWB, while FI mediates the connections between FS, DFSUB and FWB. This structured pathway model advances beyond prevalent direct-effect models in the existing literature, offering a more nuanced understanding of the interconnections among digital behaviours, financial disruptions and individual well-being outcomes.

The proposed framework provides a foundation for future empirical research, including cross-cultural and longitudinal studies, to validate and extend the identified mediating pathways across diverse populations and contexts. By organising these relationships in a structured format, the study facilitates hypothesis testing and contributes to building a more comprehensive theoretical understanding of FWB in digitally disrupted environments.

From a practical and policy standpoint, the framework highlights that enhancing FWB in a digitally driven, shock-prone economy necessitates coordinated efforts in three areas: bolstering FK, broadening FI and encouraging effective DFS usage. Policymakers can leverage these insights to craft targeted literacy programmes, improve inclusive financial infrastructure and regulate DFS in ways that support vulnerable groups. Meanwhile, managers and financial advisers can apply the model to create interventions that assist individuals in managing social media influences, preparing for shocks and using digital tools responsibly. Overall, this study offers a structured, IMB-based conceptual guide for understanding and enhancing FWB, and it calls for empirical research to validate and expand the proposed mediating pathways across various populations and contexts.

Limitations and Future Research Gap

While this study offers a comprehensive conceptual framework exploring the relationships among excessive use of SNSs, DFSUB, FS and FWB, it has several limitations that must be considered. First, the research relies solely on secondary data and insights from existing literature, which, although rich in context, lack empirical validation. The absence of primary data collection or statistical analysis restricts the ability to generalise the results or establish causality between the proposed constructs. Second, the model focuses mainly on specific mediators, FK and FI, potentially overlooking other important variables such as financial attitudes, digital literacy, or socio-cultural factors that could further enrich the framework. Moreover, the conceptual nature of the study limits its applicability to specific demographics or regions without empirical testing, and it may not account for cultural differences in financial behaviour. Lastly, the limitation is the study’s keyword selection strategy, which uses predetermined Boolean combinations of keywords related to the constructs of this study, potentially excluding relevant literature that uses synonymous or alternative terminology.

The suggested future research paths for FWB cover a broad spectrum of topics. This involves empirically validating the conceptual model with a particular focus on the mediating roles of financial knowledge and inclusion, as well as investigating other potential mediating or moderating factors. Longitudinal studies can evaluate how these relationships evolve over time, whereas cross-cultural studies might uncover variations in how factors influence FWB in different regions. Additional research should concentrate on examining the possible cultural differences in the impact of the proposed factors on FWB across various countries or regions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Shabir Hussain https://orcid.org/0000-0003-4651-5416

Amico, K. R., Barta, W., Konkle-Parker, D. J., Fisher, J. D., Cornman, D. H., Shuper, P. A., & Fisher, W. A. (2009). The information-motivation-behavioral skills model of ART adherence in a deep south HIV+ clinic sample. AIDS and Behavior, 13(1), 66–75. https://doi.org/10.1007/s10461-007-9311-y

Bashir, I., & Qureshi, I. H. (2023). Examining theories, mediators and moderators in financial well-being literature: A systematic review and future research agenda. Qualitative Research in Organizations and Management: An International Journal, 18(4), 265–290. https://doi.org/10.1108/QROM-04-2022-2314

Basu, S., S. E. Bale, C., Wehnert, T., & Topp, K. (2019). A complexity approach to defining urban energy systems. Cities, 95, 102358. https://doi.org/10.1016/j.cities.2019.05.027

Belayeth Hussain, A. H. M., Endut, N., Das, S., Chowdhury, M. T. A., Haque, N., Sultana, S., & Ahmed, K. J. (2019). Does financial inclusion increase financial resilience? Evidence from Bangladesh. Development in Practice, 29(6), 798–807. https://doi.org/10.1080/09614524.2019.1607256

Bhatia, S., & Dawar, G. (2023). The impact of financial inclusion on social and political empowerment: Mediating role of economic empowerment. Journal of the Knowledge Economy, 15(3), 13727–13744. https://doi.org/10.1007/s13132-023-01621-1

Brüggen, E. C., Hogreve, J., Holmlund, M., Kabadayi, S., & Löfgren, M. (2017). Financial well-being: A conceptualization and research agenda. Journal of Business Research, 79, 228–237. https://doi.org/10.1016/j.jbusres.2017.03.013

Buckley, R. P., & Malady, L. (2009). News extra: GSMA, contactless and mobile money. Card Technology Today, 21(7), 2. https://doi.org/10.1016/S0965-2590(09)70120-3

Bufe, S., Roll, S., Kondratjeva, O., Skees, S., & Grinstein-Weiss, M. (2022). Financial shocks and financial well-being: What builds resiliency in lower-income households? Social Indicators Research, 161(1), 379–407. https://doi.org/10.1007/s11205-021-02828-y

Chatterjee, D., Kumar, M., & Dayma, K. K. (2019). Income security, social comparisons and materialism: Determinants of subjective financial well-being among Indian adults. International Journal of Bank Marketing, 37(4), 1041–1061. https://doi.org/10.1108/IJBM-04-2018-0096

Chen, F., Du, X., & Wang, W. (2023). Can fintech applied to payments improve consumer financial satisfaction? Evidence from the USA. Mathematics, 11(2), 363. https://doi.org/10.3390/math11020363

Dare, S. E., van Dijk, W. W., van Dijk, E., van Dillen, L. F., Gallucci, M., & Simonse, O. (2023). How executive functioning and financial self-efficacy predict subjective financial well-being via positive financial behaviors. Journal of Family and Economic Issues, 44(2), 232–248. https://doi.org/10.1007/s10834-022-09845-0

Dwivedi, A., & Lewis, C. (2021). How millennials’ life concerns shape social media behaviour. Behaviour and Information Technology, 40(14), 1467–1484. https://doi.org/ 10.1080/0144929X.2020.1760938

Engels, C., Kumar, K., & Philip, D. (2021). Financial literacy and fraud detection. In Financial literacy and responsible finance in the fintech era (1st ed., pp. 124–146). Routledge. https://doi.org/10.4324/9781003169192-8

Fan, L., & Henager, R. (2025). Generational differences in financial well-being: Understanding financial knowledge, skill, and behavior. International Journal of Consumer Studies, 49(1), e70011. https://doi.org/10.1111/ijcs.70011

Fatma, M., Khan, I., Kumar, V., & Shrivastava, A. K. (2022). Corporate social responsibility and customer-citizenship behaviors: The role of customer–company identification. European Business Review, 34(6), 858–875. https://doi.org/10.1108/EBR-12-2021-0250

Faturohman, T., Megananda, T. B., & Ginting, H. (2024). Improving financial wellbeing in Indonesia: The role of social media as a mediating factor in financial behavior. Cogent Social Sciences, 10(1), 2319374. https://doi.org/10.1080/23311886.2024.2319374

Fioravanti, G., Casale, S., Benucci, S. B., Prostamo, A., Falone, A., Ricca, V., & Rotella, F. (2021). Fear of missing out and social networking sites use and abuse: A meta-analysis. Computers in Human Behavior, 122, 106839. https://doi.org/10.1016/j.chb.2021.106839

Fisher, J. D. (1992). Changing AIDS-risk behavior. Psychological Bulletin, 111(3), 455–474. https://opencommons.uconn.edu/chip_docs

French, D., McKillop, D., & Stewart, E. (2020). The effectiveness of smartphone apps in improving financial capability. European Journal of Finance, 26(4–5), 302–318. https://doi.org/10.1080/1351847X.2019.1639526

Fu, H., Manogaran, G., Wu, K., Cao, M., Jiang, S., & Yang, A. (2020). Intelligent decision-making of online shopping behavior based on internet of things. International Journal of Information Management, 50, 515–525. https://doi.org/10.1016/j.ijinfomgt.2019.03.010

Fu, J. (2020). Ability or opportunity to act: What shapes financial well-being? World Development, 128, 104843. https://doi.org/10.1016/j.worlddev.2019.104843

Gafoor, A., & Amilan, S. (2024). Fintech adoption and financial well-being of persons with disabilities: The mediating role of financial access, financial knowledge and financial behaviour. International Journal of Social Economics, 51(11), 1388–1401. https://doi.org/10.1108/IJSE-08-2023-0596

Gafoor, A., Amilan, S., & Patel, V. (2025). Financial well-being of internal migrant labours: The role of financial socialisation, financial knowledge and financial behaviour. International Journal of Social Economics, 52(1), 78–90. https://doi.org/10.1108/IJSE-01-2024-0044

García-Mata, O., & Zerón-Félix, M. (2022). A review of the theoretical foundations of financial well-being. International Review of Economics, 69(2), 145–176. https://doi.org/10.1007/s12232-022-00389-1

García-Mata, O., Zerón-Félix, M., & Briano, G. (2022). Financial well-being index in México. Social Indicators Research, 163(1), 111–135. https://doi.org/10.1007/s11205-022-02897-7

Glasford, D. E. (2008). Predicting voting behavior of young adults: The importance of information, motivation, and behavioral skills. Journal of Applied Social Psychology, 38(11), 2648–2672. https://doi.org/10.1111/j.1559-1816.2008.00408.x

Grau, S., Kleiser, S., & Bright, L. (2019). Exploring social media addiction among student millennials. Qualitative Market Research, 22(2), 200–216. https://doi.org/10.1108/QMR-02-2017-0058

Greninger, S. A., Hampton, V. L., Kitt, K. A., & Achacoso, J. A. (1996). Ratios and benchmarks for measuring the financial well-being of families and individuals. Financial Services Review, 5(1), 57–70. https://doi.org/10.1016/S1057-0810(96)90027-X

Gupta, S., Dutt, R., Sharma, A., & Sharma, B. (2024). Gamification in digital marketing: Proposing a theoretical framework based on uses and gratifications theory. BIMTECH Business Perspectives, 5(1) 9–25. https://doi.org/10.1177/25819542241246884

Gutter, M., & Copur, Z. (2011). Financial behaviors and financial well-being of college students: Evidence from a national survey. Journal of Family and Economic Issues, 32(4), 699–714. https://doi.org/10.1007/s10834-011-9255-2

Hasan, M. M., Yajuan, L., & Khan, S. (2022). Promoting China’s inclusive finance through digital financial services. Global Business Review, 23(4), 984–1006. https://doi.org/10.1177/0972150919895348

Hira, T. K., & Mugenda, O. M. (1998). Predictors of financial satisfaction: Differences between retirees and non-retirees. Journal of Financial Counseling and Planning, 9(2), 75.

Hussain, S., Gupta, S., & Bhardwaj, S. (2025a). Determinants inhibiting digital payment system adoption: An Indian perspective. Qualitative Research in Financial Markets, 17(4), 716–748. https://doi.org/10.1108/QRFM-09-2023-0223

Hussain, S., Gupta, S., & Bhardwaj, S. (2025b). Unraveling the dynamics of digital financial services adoption and digital divide: A systematic literature review and future research agenda. Journal of Global Information Technology Management, 28(2), 77–110. https://doi.org/10.1080/1097198X.2025.2480970

Hwang, H., & Park, H. I. (2023). The relationships of financial literacy with both financial behavior and financial well-being: Meta-analyses based on the selective literature review. Journal of Consumer Affairs, 57(1), 222–244. https://doi.org/10.1111/joca.12497

Jabareen, Y. (2009). Building a conceptual framework: Philosophy, definitions, and procedure. International Journal of Qualitative Methods, 8(4), 49–62. https://doi.org/10.1177/160940690900800406

Kamble, P. A., Mehta, A., & Rani, N. (2024). Financial inclusion and digital financial literacy: Do they matter for financial well-being? Social Indicators Research, 171(3), 777–807. https://doi.org/10.1007/s11205-023-03264-w

Kass-Hanna, J., Lyons, A. C., & Liu, F. (2022). Building financial resilience through financial and digital literacy in South Asia and Sub-Saharan Africa. Emerging Markets Review, 51, 100846. https://doi.org/10.1016/j.ememar.2021.100846

Kaur, G., Singh, M., & Singh, S. (2021). Mapping the literature on financial well?being: A systematic literature review and bibliometric analysis. International Social Science Journal, 71(241–242), 217–241. https://doi.org/10.1111/issj.12278

Kelly, Y., Zilanawala, A., Booker, C., & Sacker, A. (2018). Social media use and adolescent mental health: Findings from the UK Millennium Cohort Study. EClinicalMedicine, 6, 59–68. https://doi.org/10.1016/j.eclinm.2018.12.005

Ketelaar, P. E., Janssen, L., Vergeer, M., van Reijmersdal, E. A., Crutzen, R., & van ’t Riet, J. (2016). The success of viral ads: Social and attitudinal predictors of consumer pass-on behavior on social network sites. Journal of Business Research, 69(7), 2603–2613. https://doi.org/10.1016/J.JBUSRES.2015.10.151

Kim, K. T., & Lee, J. (2024). Unlocking financial well-being for people with disabilities: The importance of financial knowledge and socialization within the family context. SAGE Open, 14(2). https://doi.org/10.1177/21582440241253564

Kulshreshtha, A., Raju, S., Muktineni, S. M., & Chatterjee, D. (2023). Income shock and financial well-being in the COVID-19 pandemic: Financial resilience and psychological resilience as mediators. International Journal of Bank Marketing, 41(5), 1037–1058. https://doi.org/10.1108/IJBM-08-2022-0342

Kumar, J., & Ahuja, A. (2024). Financial inclusion: Key determinants and its impact on financial well-being. Global Business and Economics Review, 31(3), 330–353. https://doi.org/10.1504/GBER.2024.140847

Kumar, J., Rani, V., Rani, G., & Sarker, T. (2023). Determinants of the financial wellbeing of individuals in an emerging economy: An empirical study. International Journal of Bank Marketing, 41(4), 860–881. https://doi.org/10.1108/IJBM-10-2022-0475

Laila, N., Ismail, S., Mohd Hidzir, P. A., Ratnasari, R. T., & Alias, N. E. (2025). Impact of social trust, social networks, and financial knowledge on financial well-being of micro-entrepreneurs in Malaysia and Indonesia. Cogent Business and Management, 12(1). https://doi.org/10.1080/23311975.2025.2460614

Limbu, Y. B. (2017). Credit card knowledge, social motivation, and credit card misuse among college students: Examining the information–motivation–behavioral skills model. International Journal of Bank Marketing, 35(5), 842–856. https://doi.org/10.1108/IJBM-04-2016-0045

Liu, P., He, J., & Li, A. (2019). Upward social comparison on social network sites and impulse buying: A moderated mediation model of negative affect and rumination. Computers in Human Behavior, 96, 133–140. https://doi.org/10.1016/j.chb.2019.02.003

Lone, U. M., & Bhat, S. A. (2024). Impact of financial literacy on financial well-being: A mediational role of financial self-efficacy. Journal of Financial Services Marketing, 29(1), 122–137. https://doi.org/10.1057/s41264-022-00183-8

Lusardi, A. (2012). Numeracy, financial literacy, and financial decision-making (No. w17821). National Bureau of Economic Research. https://doi.org/10.3386/W17821

Lyons, A. C., & Kass-Hanna, J. (2021). A methodological overview to defining and measuring ‘digital’ financial literacy. Financial Planning Review, 4(2). https://doi.org/10.1002/cfp2.1113

Mahendru, M., Sharma, G. D., Pereira, V., Gupta, M., & Mundi, H. S. (2022). Is it all about money honey? Analyzing and mapping financial well-being research and identifying future research agenda. Journal of Business Research, 150, 417–436. https://doi.org/10.1016/j.jbusres.2022.06.034

Miranda, S., Trigo, I., Rodrigues, R., & Duarte, M. (2023). Addiction to social networking sites: Motivations, flow, and sense of belonging at the root of addiction. Technological Forecasting and Social Change, 188, 122280. https://doi.org/10.1016/j.techfore.2022.122280

Mpofu, F. Y., & Mhlanga, D. (2022). Digital financial inclusion, digital financial services tax and financial inclusion in the fourth industrial revolution era in Africa. Economies, 10(8), 184. https://doi.org/10.3390/ECONOMIES10080184

Nandru, P., Chendragiri, M., & Velayutham, A. (2021). Examining the influence of financial inclusion on financial well-being of marginalized street vendors: An empirical evidence from India. International Journal of Social Economics, 48(8), 1139–1158. https://doi.org/10.1108/IJSE-10-2020-0711

Netemeyer, R. G., Warmath, D., Fernandes, D., & Lynch, J. G. (2018). How am I doing? Perceived financial well-being, its potential antecedents, and its relation to overall well-being. Journal of Consumer Research, 45(1), 68–89. https://doi.org/10.1093/jcr/ucx109

Nizam, K., & Rashidi, M. Z. (2025). Barriers to digital financial inclusion and digital financial services (DFS) in Pakistan: A phenomenological approach. Qualitative Research in Financial Markets, 17(2), 251–274. https://doi.org/10.1108/QRFM-11-2023-0271

Parayil Iqbal, U., Jose, S. M., & Tahir, M. (2023). Integrating trust with extended UTAUT model: A study on Islamic banking customers’ m-banking adoption in the Maldives. Journal of Islamic Marketing, 14(7), 1836–1858. https://doi.org/10.1108/JIMA-01-2022-0030

Rahman, S. A., Alam, M. M. D., & Taghizadeh, S. K. (2020). Do mobile financial services ensure the subjective well-being of micro-entrepreneurs? An investigation applying UTAUT2 model. Information Technology for Development, 26(2), 421–444. https://doi.org/10.1080/02681102.2019.1643278

Rana, N. P., Luthra, S., & Rao, H. R. (2020). Key challenges to digital financial services in emerging economies: The Indian context. Information Technology and People, 33(1), 198–229. https://doi.org/10.1108/ITP-05-2018-0243

Riitsalu, L., & Murakas, R. (2019). Subjective financial knowledge, prudent behaviour and income: The predictors of financial well-being in Estonia. International Journal of Bank Marketing, 37(4), 934–950. https://doi.org/10.1108/IJBM-03-2018-0071

Riitsalu, L., Sulg, R., Lindal, H., Remmik, M., & Vain, K. (2024). From security to freedom— The meaning of financial well-being changes with age. Journal of Family and Economic Issues, 45(1), 56–69. https://doi.org/10.1007/s10834-023-09886-z

Ringelstein, D., & Patel, K. (2023). A conceptual framework for informatics. E-Journal of Business Education and Scholarship of Teaching, 17(1), 9–14. https://eric.ed.gov/?id=EJ1376059

Salignac, F., Hamilton, M., Noone, J., Marjolin, A., & Muir, K. (2020). Conceptualizing financial wellbeing: An ecological life-course approach. Journal of Happiness Studies, 21(5), 1581–1602. https://doi.org/10.1007/s10902-019-00145-3

Santini, F. D. O., Ladeira, W. J., Mette, F. M. B., & Ponchio, M. C. (2019). The antecedents and consequences of financial literacy: A meta-analysis. International Journal of Bank Marketing, 37(6), 1462–1479. https://doi.org/10.1108/IJBM-10-2018-0281

Seacat, J. D., & Northrup, D. (2010). An information-motivation-behavioral skills assessment of curbside recycling behavior. Journal of Environmental Psychology, 30(4), 393–401. https://doi.org/10.1016/j.jenvp.2010.02.002

Shang, S. S. C., Wu, Y. L., & Sie, Y. J. (2017). Generating consumer resonance for purchase intention on social network sites. Computers in Human Behavior, 69, 18–28. https://doi.org/10.1016/J.CHB.2016.12.014

She, L., Ma, L., Voon, M. L., & Lim, A. S. S. (2023). Excessive use of social networking sites and financial well-being among working millennials: A parallel-serial mediation model. International Journal of Bank Marketing, 41(1), 158–178. https://doi.org/10.1108/IJBM-04-2022-0172

She, L., Rasiah, R., Waheed, H., & Pahlevan Sharif, S. (2021). Excessive use of social networking sites and financial well-being among young adults: The mediating role of online compulsive buying. Young Consumers, 22(2), 272–289. https://doi.org/10.1108/YC-11-2020-1252

Shell, D. F., Newman, I. M., Perry, C. M., & Folsom, A. R. B. (2011). Changing intentions to use smokeless tobacco: An application of the IMB model. American Journal of Health Behavior, 35(5), 568–580. https://doi.org/10.5993/AJHB.35.5.6

Shim, S., Xiao, J. J., Barber, B. L., & Lyons, A. C. (2009). Pathways to life success: A conceptual model of financial well-being for young adults. Journal of Applied Developmental Psychology, 30(6), 708–723. https://doi.org/10.1016/j.appdev.2009.02.003

Sonali, S., Hussain, S., Gupta, S., & Bhardwaj, S. (2025). A helping hand in banking: How off-site customer-to-customer interactions impact the mobile banking usage behaviour and financial well-being. International Journal of Bank Marketing, 1–29. https://doi.org/10.1108/IJBM-02-2025-0125

Sun, L., Small, G., Huang, Y. H., & Ger, T. B. (2022). Financial shocks, financial stress and financial resilience of Australian households during COVID-19. Sustainability (Switzerland), 14(7), 3736. https://doi.org/10.3390/su14073736

Teo, L. X., Leng, H. K., & Phua, Y. X. P. (2019). Marketing on Instagram: Social influence and image quality on perception of quality and purchase intention. International Journal of Sports Marketing and Sponsorship, 20(2), 321–332. https://doi.org/10.1108/IJSMS-04-2018-0028

Thorisdottir, I. E., Sigurvinsdottir, R., Asgeirsdottir, B. B., Allegrante, J. P., & Sigfusdottir, I. D. (2019). Active and passive social media use and symptoms of anxiety and depressed mood among Icelandic adolescents. Cyberpsychology, Behavior, and Social Networking, 22(8), 535–542. https://doi.org/10.1089/cyber.2019.0079

Thoumrungroje, A. (2018). A cross-national study of consumer spending behavior: The impact of social media intensity and materialism. Journal of International Consumer Marketing, 30(4), 276–286. https://doi.org/10.1080/08961530.2018.1462130

Tsai, W. H. S., & Men, L. R. (2017). Consumer engagement with brands on social network sites: A cross-cultural comparison of China and the USA. Journal of Marketing Communications, 23(1), 2–21. https://doi.org/10.1080/13527266.2014.942678

Tulcanaza-Prieto, A. B., Cortez-Ordoñez, A., Rivera, J., & Lee, C. W. (2025). Is digital literacy a moderator variable in the relationship between financial literacy, financial inclusion, and financial well-being in the Ecuadorian context? Sustainability (Switzerland), 17(6), 2476. https://doi.org/10.3390/su17062476

Vishwakarma, P. (2024). Impact of womens financial inclusion and financial attitude on their financial well-being. Journal of Commerce and Accounting Research, 13(1), 1–12. https://doi.org/10.21863/JCAR/2024.13.1.001

Vlaev, I., & Elliott, A. (2014). Financial well-being components. Social Indicators Research, 118(3), 1103–1123. https://doi.org/10.1007/s11205-013-0462-0

Wilcox, K., & Stephen, A. T. (2013). Are close friends the enemy? Online social networks, self-esteem, and self-control. Journal of Consumer Research, 40(1), 90–103. https://doi.org/10.1086/668794

Xiao, J. J., Chen, C., & Chen, F. (2014). Consumer financial capability and financial satisfaction. Social Indicators Research, 118(1), 415–432. https://doi.org/10.1007/s11205-013-0414-8

Yang, T., & Zhang, X. (2022). Fintech adoption and financial inclusion: Evidence from household consumption in China. Journal of Banking and Finance, 145, 106668. https://doi.org/10.1016/j.jbankfin.2022.106668

Zhang, Y., & Fan, L. (2024). The nexus of financial education, literacy and mobile fintech: Unraveling pathways to financial well-being. International Journal of Bank Marketing, 42(7), 1789–1812. https://doi.org/10.1108/IJBM-09-2023-0531