BIMTECH Business Perspectives

Search

Search

Sunny1 , Garima Dalal1 and Sonia1

, Garima Dalal1 and Sonia1

1 IMSAR Maharshi Dayanand University, Rohtak, Haryana, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This review article examines merger and acquisition (M&A) activity in the banking sector, driven by the expanding use of bibliometric evaluations in finance and global consolidation trends. The systematic review portion of the study was conducted in accordance with the PRISMA guidelines, ensuring transparent identification, screening, eligibility, and inclusion of the studies. Using co-citation, co-authorship, and keyword co-occurrence network analysis, we present a novel and integrative literature review that not only maps influential journals, authors, papers, and countries but also critically synthesises existing knowledge, highlights theoretical and methodological gaps, and proposes future research directions for the field. Analysing 7,734 papers from the Scopus database (2000–2023) highlights the dominance of wealthy nations, which creates opportunities for the study of risk-return dynamics and regulatory changes in emerging economies. The project is the first of its kind in the field of research on bank mergers, and it will contribute to a reservoir of literature by identifying prospective research areas using Scopus database articles.

Banks, merger and acquisition, credit risk, systemic risk, bibliographic analysis

Introduction

Mergers and acquisitions (M&A) serve as a strategic approach for companies seeking to reorganise or unify their business operations.

The statistics associated with these phenomena are alarming, as indicated by studies conducted by Ferreira et al. (2014), Moschieri and Campa (2014) and Homburg and Bucerius (2005).

M&A are widely recognised as a feasible approach to reorganising corporate business operations. Following the economic decline triggered by the COVID-19 pandemic, M&A activities have reached unprecedented levels, with analysts projecting a consistent upward trajectory in the foreseeable future. This surge is primarily attributed to the dynamic regulatory landscape. In contrast, scholarly investigations of M&A focus on their financial effectiveness, economic dynamics, and implications across national boundaries. A considerable body of evidence suggests that a substantial number of M&A fail to yield successful outcomes (Weber et al., 2014). Various studies have estimated failure rates for M&A activities to be within the range of 60%–80% (Homburg & Bucerius, 2005; Papadakis & Thanos, 2010; Schoenberg, 2006; Thorbjørnsen & Dahlén, 2011).

Reddy et al. (2025) revealed significant clustering among Indian banks, particularly within public sector institutions and large private sector banks. Their study demonstrates that these institutions exhibit strong positive correlations in credit exposure patterns, which may pose systemic risks to the financial system. Their findings suggest that such highly correlated credit exposures heighten contagion risk, whereby distress in one institution can spill over across the cluster, thereby amplifying financial instability. Soedarmono et al. (2017) analysed how abnormal loan growth can affect bank systemic risk in emerging markets from a sample of publicly traded commercial banks in the Asia Pacific region and revealed that higher abnormal loan growth increases bank systemic risk 1 year ahead. However, the results were conditional on the quality of credit information sharing at the country level.

Credit risk-taking is increased in the post-merger period if the banks are state-owned, have a deficient internal governance mechanism, and are part of a banking system with quality issues in supervision. The post-M&A performance is unaffected by ownership or governance but is improved by a lackadaisical oversight framework (Asandului et al., 2016). While the literature on M&A is expected to grow significantly over time, we are concerned with exploring (a) the areas on which contemporary studies are focused and (b) the scant areas on which future research should focus. In their study titled ‘Bank mergers: The cyclical behaviour of regulation, risk and returns’, Hassan and Giouvris (2021) revealed that large acquiring banks decrease systemic risk contribution in cross-border M&A with non-bank financial institutions. According to Ngo (2019), there is a positive and direct relationship between banks’ default risk and their Marginal Expected Shortfall (MES) and idiosyncratic risk during the pre-merger period. Later on, in relation to the impact of bank mergers, no significant associations were observed between changes in default risk and changes in MES or between changes in default risk and changes in beta. This underscores that consolidation is not a ‘risk cure’—the core vulnerabilities of banks persist regardless of M&A activity. In a study conducted by Nguyen et al. (2019), empirical evidence was presented to support the occurrence of a risk shift characterised by a positive (negative) trend. This shift was observed when the equity beta of the acquiring firm was lower than (higher than) the beta of the target firm. During the initial 5 and 10 days after the announcement, the cumulative abnormal returns exhibit a negative and statistically significant pattern. However, these negative abnormal returns diminish rapidly when beta adjustments are incorporated in the estimation of abnormal returns.

Concerning cross-country issues, Weiß et al. (2014) examine the systemic risk effects of bank mergers to assess ‘concentration fragility’ and find clear evidence of a substantial increase in the merging banks’, the combined banks’, and their competitors’ contributions to systemic risk following mergers. In contrast, Van Dellen et al. (2018) investigated the systemic risk implications of bank mergers from 1998 to 2015, including the post–global financial crisis period, and found that on average, M&A do not alter acquiring banks’ contribution to systemic risk, even in cross-border or cross-industry deals. However, factors such as payment method, target status, relative size, rule of law, and political stability significantly influence changes in systemic risk. Brealey et al. (2019) found that short-term increases in acquirer risk after mergers occur only in the first few mergers conducted by the same acquirer and only in systematic risk. Using a novel method for quantifying the long-term effect, it was found that the change in risk associated with mergers is nonlinearly dependent on the acquirer’s total number of mergers.

Studies on M&A are no exception to the literature’s predominant concentration on the banking sector. However, a few research examined Acquirers of listed versus unlisted firms: factors in different legal and institutional settings (Feito-Ruiz & Menéndez-Requejo, 2013), despite different effects found for the impact of payment methods and acquisition modes on risk and revenue metrics by Dube and Glasscock (2006), and the alterations in bank credit risk subsequent to a merger (Knapp & Gart, 2014). The credit risk performance of private banks is significantly higher than that of government banks, which is not surprising given the operational freedom enjoyed by private banks and their objective of achieving superior performance. The government banks suffer due to interference from different agencies of government (Sharifi et al., 2019).

The current pandemic and the recent global financial crisis might have sparked significant consolidation waves in the fiscal sector that are distinct from earlier ones with regard to their geographic extent and the specific products or services involved. Hence, it is imperative to conduct a bibliometric analysis that investigates the dynamics and crucial determinants of M&A within the financial industry.

Bibliometric analysis is a widely used instrument for evaluating scientific output that necessitates examining multiple viewpoints (Bojovi.png) et al., 2014). However, the task of analysing a substantial volume of systematic data and recognising prevailing patterns poses an enormous challenge. Nevertheless, this analysis prompts further investigation into the voids and potential avenues for novel theoretical frameworks and empirical discoveries (Botelho et al., 2011). In accordance with the findings of Liu et al. (2014), this methodology effectively demonstrates the dynamics of publication patterns, along with the emergence of new disciplines and their evolution over time. As a result, these domains can be configured utilising efficient methodologies and specialised software. The bibliometric approach, when combined with content analysis, provides a comprehensive lens through which the influential and intellectual structure of a research field can be examined. This dual perspective not only maps patterns of scholarly output and citation networks but also uncovers thematic trends, key contributors, and the evolution of ideas over time. By integrating quantitative bibliometric indicators with qualitative content insights, researchers gain a broad view of how knowledge is produced, disseminated, and interconnected, thereby offering a deeper understanding of the dynamics shaping the field (Chiaramonte et al., 2023). To be more specific, this methodology assists us in finding answers to the study questions listed below:

et al., 2014). However, the task of analysing a substantial volume of systematic data and recognising prevailing patterns poses an enormous challenge. Nevertheless, this analysis prompts further investigation into the voids and potential avenues for novel theoretical frameworks and empirical discoveries (Botelho et al., 2011). In accordance with the findings of Liu et al. (2014), this methodology effectively demonstrates the dynamics of publication patterns, along with the emergence of new disciplines and their evolution over time. As a result, these domains can be configured utilising efficient methodologies and specialised software. The bibliometric approach, when combined with content analysis, provides a comprehensive lens through which the influential and intellectual structure of a research field can be examined. This dual perspective not only maps patterns of scholarly output and citation networks but also uncovers thematic trends, key contributors, and the evolution of ideas over time. By integrating quantitative bibliometric indicators with qualitative content insights, researchers gain a broad view of how knowledge is produced, disseminated, and interconnected, thereby offering a deeper understanding of the dynamics shaping the field (Chiaramonte et al., 2023). To be more specific, this methodology assists us in finding answers to the study questions listed below:

The data presented here were extracted from Scopus-indexed publications published between 2000 and 2023 to ensure both historical depth and contemporary relevance. From the early 2000s onward, bibliometric databases provide comprehensive coverage, allowing for consistent data collection. This timeframe encompasses critical events such as the 2008 Global Financial Crisis, subsequent regulatory reforms, and the rise of digital banking, all of which significantly shaped scholarly discourse on bank mergers and risk. By extending the analysis to 2023, the study captures the most recent intellectual contributions, offering a holistic view of the field’s evolution.

We chose Scopus index as it covers more journals than WoS, especially in social sciences, business, and economics. Scopus database is the world’s largest abstracting and indexing database, and updates daily and is comparatively more up-to-date with trending topics such as the Web of Science, which updates weekly (Burnham, 2006; de Moya-Anegón et al., 2007). Moreover, sufficient literature published in reputed journals uses the Scopus database for bibliometric and content analysis (Goodell et al., 2021; Patel et al., 2022). Our article is organised as follows. The technique and data selection procedure are explained in the second section. The third section discusses our findings, whereas the fourth section illustrates network visualisations of the M&A literature. The fifth section summarises limitations and makes recommendations for future research, and the sixth section concludes our article.

Data and Methodology

Methodology Employed

Price (1965) first proposed bibliometrics, which seeks to comprehend scholarly networks across articles. Following the aforementioned methodological structure, we analyse the following dimensions: (a) Bibliographic analysis of citation, (b) bibliographic analysis of co-authorship and (c) keyword/cartographic analysis.

We use VOS viewer software to analyse the data and derive visualisation networks (Baker, Kumar, & Pandey, 2020; Baker, Kumar, & Pattnaik, 2020; Khan et al., 2020; Van Eck & Waltman, 2010) as it is highly renowned and extensively utilised by researchers engaged in bibliometric analyses (Baker, Kumar, & Pandey, 2020; Baker, Kumar, & Pattnaik, 2020; Khan et al., 2020; Paltrinieri et al., 2023).

Data Selection

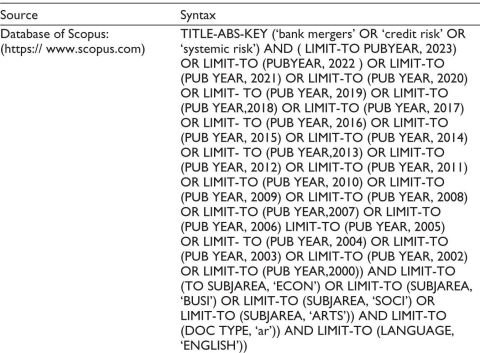

The process of sample selection encompasses three distinct stages. The initial phase entails the selection of a database from which data will be extracted for the purpose of conducting bibliometric analysis. In this review, we have chosen to utilise the Scopus database, which is widely recognised as a dependable source for conducting bibliometric analysis. Notably, Scopus surpasses WoS in terms of its extensive size, making it particularly advantageous for mapping out niche research domains that may have been insufficiently represented in the past. (Zupic & Cater, 2015). During the second stage, a literature search is conducted using relevant keywords. A comprehensive search was conducted in the entire database, encompassing articles for the period 2000–2023 as it encompasses pivotal events such as the 2008 Global Financial Crisis, the European debt crisis, Brexit, the COVID-19 pandemic, and recent banking stresses. These milestones profoundly influenced both merger activity and risk scholarship, making this timeframe essential for mapping the intellectual landscape. We searched for ‘bank merger’, ‘credit risk’, and ‘systemic risk’ in the Title, Abstract, and Keywords columns. This process resulted in a total of 14,886 articles.

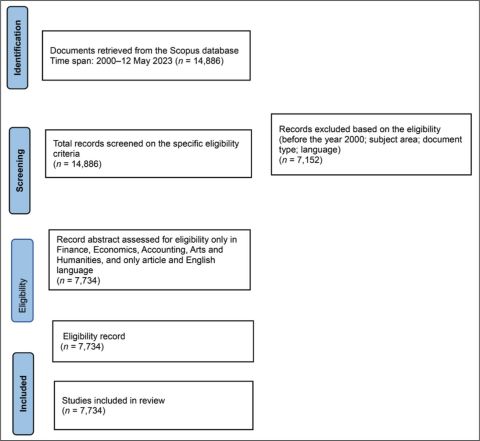

The PRISMA approach review procedure is depicted in Figure 1.

Figure 1. Prisma Flow Diagram in the Identification and Screening of Publications on Bank Mergers, Credit Risk, and Systemic Risk from 2000 to 12 May 2023.

The acronym PRISMA refers to the ‘Preferred Reporting Items for Systematic Reviews and Meta-Analyses’ set of guidelines. Data are extracted and analysed from the literature in a methodical and transparent manner with the use of this methodology (Moher et al., 2010; Paul & Dhiman, 2021).

Identification: Identification encompasses an exhaustive examination of a desktop search. The first step was a desktop search of Scopus, the largest and most comprehensive database of scholarly publications and studies. The time frame for the search was set to go from 2000 to 27 May 2023. The next step was to identify the bank merger-related keywords that would aid in achieving the study’s objectives. When searching for papers by title, abstract, or keywords, a list of pertinent search phrases (Table 1) was used, and the initial results returned 14,886 papers.

Table 1. The Scopus Search Syntax Used Is as Follows.

Screening: Due to the small number of articles published prior to the year 2000, we exclude them from the screening process. Furthermore, we have chosen to include only review articles/papers in English, and the publication must be in the fields of ‘Economics’, ‘Econometrics’, ‘Finance’, ‘Business Management’, ‘Accounting’, ‘Social sciences’, and ‘arts’. In this phase, 7,152 documents were eliminated based on the application of predetermined criteria, and a total of 7,734 articles and studies were found relevant.

Eligibility: The current phase of the PRISMA methodology holds significant importance. The term ‘eligible papers’ refers to the number of research articles that meet certain predetermined criteria established by the researcher. A total of 7,734 papers have been deemed eligible for inclusion in the study, as per the aforementioned criteria.

Included: The ultimate database of the study consisted of 7,734 studies. The aforementioned studies were taken into account for the purpose of conducting a citation analysis, with the aim of identifying the most influential authors, sources, organisations, and countries within this particular field of study.

Findings

General Data and Performance Evaluation

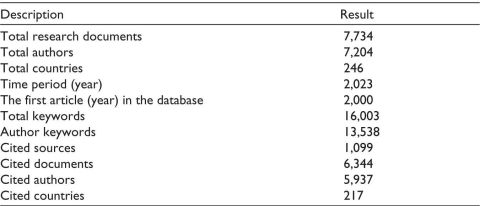

The primary structure of the collated data is presented in Table 2. Our publications span the years 2000 to 27 May 2023 and include 7,734 articles by 7,204 authors.

Table 2. Descriptive Statistics.

Highly Prominent Outlook of Bank Mergers

Table 2 provides a synopsis of the 7,734 articles that were found. The 7,734 papers were from 1,099 publications, had 7,204 authors, 16,003 keywords, and represented 246 countries. The subsequent sections of this article present a comprehensive overview of the existing literature on bank mergers, focusing on the bibliographic details of the sources.

Highly Prominent Authors

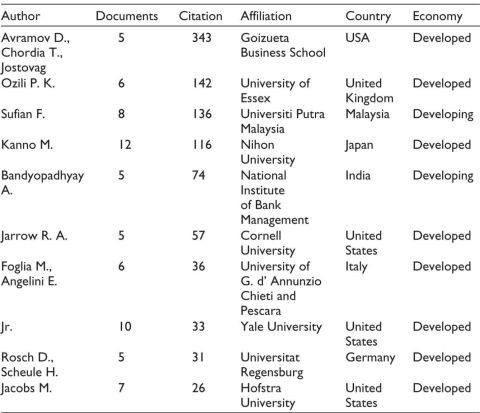

As a criterion for identifying highly influential authors, the authors of at least five publications with a minimum of five citations were selected. 13 out of 7,204 authors satisfy the criteria. Table 3 presents a compilation of authors who have garnered the highest number of citations for their published research on bank mergers. The individuals Avramov D., Chordia T., and Jostovag have made the highest number of contributions, with a total of five documents and 343 citations. Following closely is Ozili P. K., who has received six documents and 142 citations. On the other hand, it is noteworthy to mention that Kanno M. has emerged as the most prolific author in the domain of bank mergers, with a cumulative publication count of 12 documents. However, their work was less cited than that of others.

Table 3. Highly Prominent Authors.

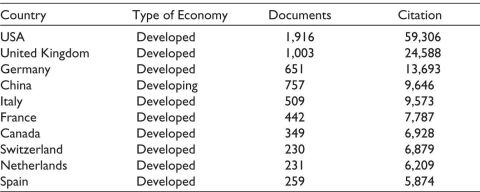

Highly Prominent Countries

Table 4 presents the citations categorised by nations, with a criterion of at least 5 documents and 10 citations, revealing that only 86 of the 246 countries met the condition. Table 4 displays the world’s 10 most prominent and cited nations. In the categories of documents (1,916) and citations (59,306), the United States, a country with a ‘developed’ status, came in first. In addition, the United Kingdom ranked second with 1,003 documents containing 24,588 citations, followed by Germany, China, and others.

Table 4. Highly Prominent Countries.

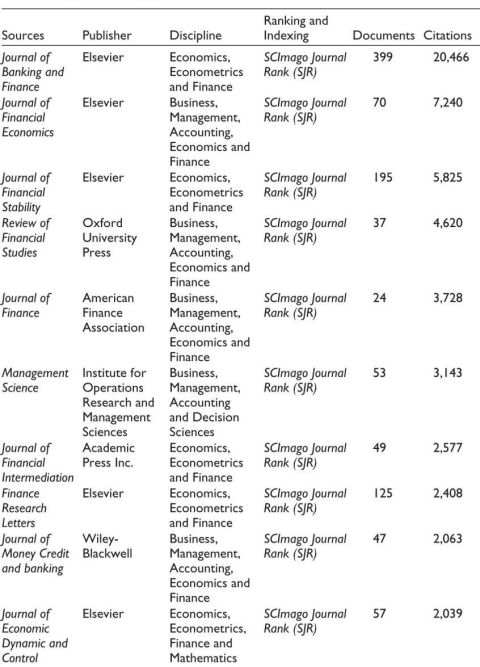

Highly Prominent Journals

From sources containing at least five documents and at least five citation sources, a comprehensive citation map was generated. There were only 13 sources out of 189 that fulfilled the criteria. Table 5 lists the top 10 journals with the most citations. The Elsevier publication Journal of Banking and Finance has the highest impact factor, with 20,466 citations over 399 documents, and is ranked with SCImago Journal Rank (SJR). The second most cited publication was Elsevier’s Journal of Financial Economics, a multidisciplinary journal with 7,240 citations and 70 documents cited. Elsevier’s Journal of Financial Stability contains 5,825 citations and 195 documents in total.

Table 5. Highly Prominent Journals.

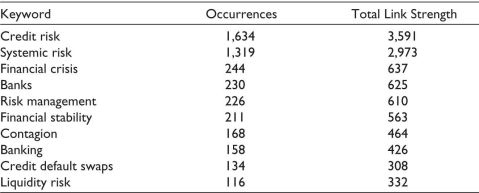

Highly Prominent Keywords

To facilitate analysis, the authors constructed a keyword co-occurrence map utilising the terms they provided. Table 6 presents a compilation of keywords that are found within a proximity of five instances of each other, accompanied by their corresponding thresholds. Out of the total of 13,538 keywords, only 972 keywords were able to meet the requirement. It was inevitable that the term ‘credit risk’ would have the most occurrences, given that the purpose of this study is to identify credit and systemic risk in the domain of bank mergers. Credit risk was mentioned 1,634 times in the articles, with a total linkage strength of 3,591. This illustrates the heightened academic curiosity about credit risk in bank mergers, which promotes fresh investigation in the aforementioned area. Systemic risk emerged as the second most frequently encountered term, with a total link strength of 2,973 and 1,319 occurrences. Followed by financial crises exhibiting a total link strength of 637 and 244 occurrences. Additional terms in the top 10 keywords list were ‘banks’, ‘risk management’, ‘financial stability’, ‘contagion’, ‘banking’, ‘g21’ and ‘liquidity risk’.

Table 6. Highly Prominent Author’s Keywords.

Network Visualisation of M&A Literature

Document Co-citation Analysis

The initial co-citation analysis examined the cartel of documents related to the consolidation of banks. The utilisation of document co-citation analysis enables researchers to ascertain the underlying conceptual framework of multiple documents within a particular academic domain. Consequently, we will be able to figure out which documents characterise the conceptual framework of bank mergers. A total of 264,028 citations were generated, with 243 of them meeting the criteria of at least 20 quotations per work (Figure 2). Each of the nodes represented the number of citations per text as well as the scope of a single reference. This relationship was a co-citation. Similar-coloured nodes belonged to the same cluster. As is evident in Figure 2, the VOS viewer’s algorithm identified six main clusters (red, green, yellow, blue, purple, and sky blue).

Figure 2. Document Co-citation Network of Bank Mergers.

The red cluster represented significant publications about bank mergers. The majority of the discussion in these documents centred on constructing the concept of bank mergers. For instance, the work of Allen and Gale (2004), titled ‘Competition and financial stability’, which is part of the red cluster has investigated numerous kinds of competition and financial stability models, including ‘general equilibrium models’ of financial intermediaries and markets, ‘agency models’, ‘spatial competition models’, ‘Schumpeter competition’, and ‘contagion’. Similarly, more studies such as ‘Econometric measures of connectedness and systemic risk in the finance and insurance sectors’ (Billio et al., 2012) and ‘Systemic risk: a survey’ (De Bandt & Hartmann, 2000) constituted the main part of the red cluster.

The green cluster had 42 items. The critical studies that comprised the green cluster were ‘Bank governance, regulation, and risk-taking’ (Laeven & Levine, 2009), ‘Deregulation, market power and risk behaviour in Spanish banks’ (Salas & Saurina, 2003) and ‘Initial conditions and moment restrictions in dynamic panel data models’ (Blundell & Bond, 1998).

Third, the blue cluster contains 40 items ‘On the pricing of corporate debt: The risk structure of interest rates’ (Merton, 1974) and ‘Term structures of credit spreads with incomplete accounting information’ (Duffie & Lando, 2001).

The yellow cluster is the fourth cluster, which includes studies ‘Systemic risk in financial systems’ (Eisenberg & Noe, 2001), ‘Capital shortfall: A new approach to ranking and regulating systemic risks’ (Acharya et al., 2012) and many more. Fifth cluster is the purple cluster includes studies like ‘Systemic risk and stability in financial networks’ (Acemoglu et al., 2015), ‘Measuring systemic risk’ (Acharya et al., 2017), etc. and last cluster is sky-blue cluster which contains studies ‘The pricing of options and corporate liabilities’ (Black & Scholes, 1973), ‘Financial ratios, discriminant analysis and the prediction of corporate bankruptcy’ (Altman, 1968) and others.

Co-citation Analysis of Authors

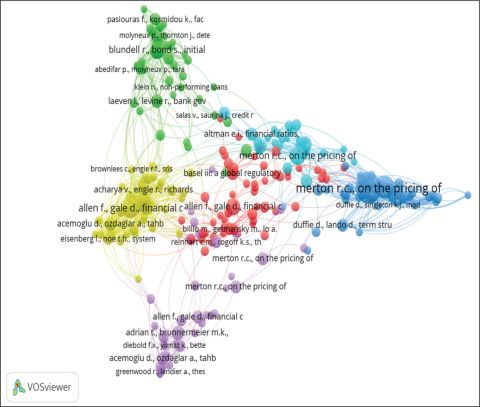

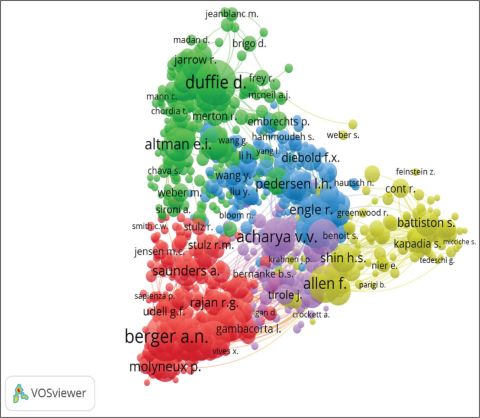

The author’s bank merger co-citation network was examined in the second co-citation analysis. In author co-citation analysis, the key decision is which authors should be tracked. As stated previously, co-citation analysis is used to map the conceptual framework of a subject or field. Author co-citation analysis is used to map/determine the conceptual framework of authors (major contributors who have published a number of papers related to the field) in the field of bank mergers. We compiled a sample of 133,967 authors after analysing the reference data extracted from our 7,715 papers. Following this, only authors with at least 20 citations were taken, resulting in a total of 5,349 authors. For each of the 5,349 authors, the cumulative co-citation link strength with other authors was computed. Following the selection of the writers who had the highest overall link strength, an analysis was carried out on these one thousand contributions. Figure 3 depicts the resulting network, which includes the formation of specific clusters.

Figure 3. Co-citation Network of Authors of Bank Mergers.

A total of five clusters were identified through co-citation analysis. The red cluster is the first main cluster, revealing the writers who have contributed to the understanding and expansion of numerous bank merger dimensions (e.g., Berger A. N., Saunders A., Shleifer A., Rajan R. G., Laeven L.; Laeven & Valencia, 2013). For instance, Berger (2018). The benefits and costs of the TARP bailouts: A critical assessment. Quarterly Journal of Finance, 8(02), 1850011. The nodes of the same colour indicate how the work of other individuals within the same cluster is connected.

The green cluster identifies numerous authors who have contributed either directly or indirectly to the study to discover how bank mergers benefited the organisation and what their likely outcomes were. This includes the writings of authors like Duffie (2005), who found credit risk modelling with affine processes. On the other hand, Altman (2018) stated a 50-year retrospective on credit risk models, the Altman Z-score family of models, and their applications to financial markets and managerial strategies. Merton and Thakor (2019) discussed Customers and investors: a framework for understanding the evolution of financial institutions.

The blue cluster depicts the work of a highly prominent author named Brunnermeier and Cheridito (2019). Measuring and allocating systemic risk. Risk. with 111 citations.

Various authors, such as Pedersen L. H., Engle R., Zhou H., and the cluster, including a great deal of others. They are the ones who have strived to elucidate the subject more thoroughly. Two additional minor clusters (yellow and purple), in addition to the three clusters mentioned above, were found. These clusters comprised the research conducted by the authors, including Adrian T., J. Tirole, F. Allen and Shin H. S. represent the work of authors, such as Acharya et al. (2007) and Battiston et al. (2016), and a few others, whose studies were not specifically centred on bank mergers, were also included. Nevertheless, due to the similarity in their respective areas of study, specifically in the area of finance, the writers made reference to the scholarly contributions of other authors who also operated within this field, thereby illustrating the interconnectedness between them.

Cluster Analysis

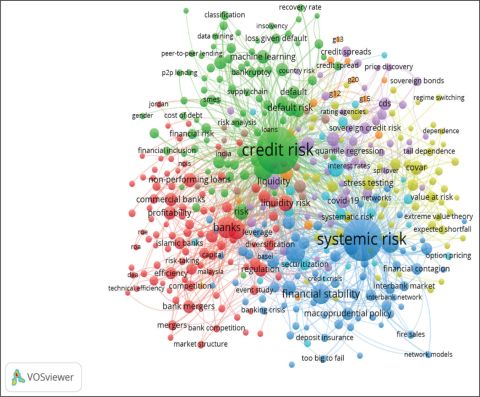

Keyword Cluster Analysis

The researchers employed VOS viewer software to perform a keyword cluster analysis with the aim of identifying the predominant research streams. Figure 4 depicts the co-occurrence map. Bank mergers are typically associated with concepts such as credit risk, systemic risk, banks, financial stability, regulation, etc. Figure 4 displays a visual depiction of the keywords that have appeared, adhering to the criterion of a minimum of 10 occurrences. Through the utilisation of term repetition, the identification of eight prominent clusters (namely, red, green, yellow, blue, purple, orange, sky blue, and brown). The first red cluster (‘banks’ and ‘bank mergers’) included terms like ‘banks’, ‘liquidity risk’, ‘regulation’, ‘profitability’, and several others. The cluster effectively demonstrates the variables employed by various writers to examine the relationships between them. The notable studies were those carried out by Goyal and Joshi (2011) and Kress (2020). The green cluster, featuring bank merger and credit risk, is the second significant cluster to form. The relationship between bank mergers and credit risk is well-depicted in the literature. Bank mergers and credit risk are related, according to numerous studies (Bonaccorsi di Patti & Gobbi, 2003; Knapp & Gart, 2014). This cluster also included other important phrases like credit risk, risk, financial risk, and default risk.

Figure 4. Co-occurrence Network of Author Keyword.

The blue cluster (bank merger and systemic risk) represents the third cluster. Systemic risk, financial stability, too big to fail, and banking crises are the keywords that make up the cluster. It is important to note that the work of Weiß et al. (2014) has been crucial in the development of numerous systemic risk dimensions. In addition, a large number of authors, including Molyneux et al. (2014) and Saunders and Walter (2012), have discovered a positive correlation between bank mergers and the terms found in the blue cluster after studying the cluster’s keywords.

The yellow cluster is the fourth cluster, which includes the terms value at risk, extreme value theory, stress testing, and many others. COVID-19, credit ratings, credit spreads, country risk, and many other items are included in the purple fifth cluster. The sky-blue cluster, which comprises credit default swaps, structural models, counterparty credit risk, etc., is the sixth cluster. The seventh cluster, known as the orange cluster, is made up of the G11, G20, G31, capital regulation, and European banks. The final major cluster discovered using keyword occurrence mapping, the brown cluster (bank mergers and financial institutions), also contains India, regulatory capital, asset quality, etc.

Limitations of the Study

It is possible that the bibliometric citation analysis is one of the study’s flaws. This study focused mostly on highly cited papers; hence, articles with citation counts below the threshold restrictions can be ignored. It is suggested that in the future, researchers should cover more recent publications by trying out the framework with new methods, software, and databases like the Web of Science, Google Scholar, JSTOR, and others. Second, there may be other factors at play besides bank mergers, bank credit, and systemic risk that make it difficult to establish a causal relationship among these outcomes. A strong causal link between bank mergers and their influence on bank credit and systemic risk can be hard to demonstrate, despite the fact that statistical approaches can help to control some of these issues.

Future Research Agenda

Based on the discovered gaps in the literature, this section suggests new lines of inquiry. First, according to our research, while affluent nations have already made significant progress in this area, greater attention should be directed toward emerging economies, where risk-return dynamics and regulatory changes remain underexplored. Second, the relationship between M&A activity and systemic risk warrants deeper investigation, particularly in light of post-crisis financial stability concerns. Third, methodological innovation is needed, with advanced techniques such as machine learning and network analysis offering new insights. Fourth, the frequency of cross-border bank mergers has increased in recent years, and the effect of these mergers on bank credit and systemic risk is an essential area for future study. Finally, the rise of fintech and digital banking presents opportunities to examine how technological disruption influences consolidation and systemic risk. This research could aid policymakers in gaining a better understanding of the potential advantages and disadvantages of cross-border bank mergers and in formulating policies to mitigate the potential risks.

Conclusion

This article aimed to investigate the bibliometric characteristics of the literature pertaining to M&A within the banking sector. The Scopus database was chosen as a reliable source for conducting bibliometric analysis. A total of 14,886 research publications on bank mergers, specifically focusing on the period from 2000 to 2023, were identified. We found 7,734 papers from 1,099 publications, had 7,204 authors with 16,003 keywords, and represented 246 countries provide a comprehensive overview of the current state of the field and offering insights into potential avenues for future research. The utilisation of keyword co-occurrence analysis facilitated the exploration of novel themes in the field of research. This approach enabled us to establish connections between crucial research domains and clusters of disciplines. The identification of keywords through bibliometric analysis of the most recently cited works is believed to exert influence on the advancement of research in the field of bank mergers. The most influential identified terms were credit risk, systemic risk, financial crises, and banks. The United States, the United Kingdom, Germany, and China are the leading countries in terms of overall publications and specified citations. The key journals are the Journal of Banking and Finance, Journal of Financial Economics, and Journal of Financial Stability. Avramov D., Chordia T., Jostovag, Ozili P. K., and Sufian F. are the authors with the most citations. The authors’ co-citation network demonstrated that the individuals who garnered the highest number of citations and possessed the greatest total link strength were also the most influential figures within their respective research domain. Specifically, the authors Berger A. N., Saunders A., Duffie D., and Acharya V. V. Authors such as Duffie (2005) discovered credit risk modelling with affine processes, Altman (2018) conducted a comprehensive analysis on credit risk models, the Altman Z-score family of models and their utilisation in financial markets and managerial contexts over a span of 50 years. The existing body of literature predominantly focuses on the economic outcomes, factors influencing them, and the interplay across national borders. These areas of study are primarily rooted in the disciplines of business finance, economics, management, and business. Bank mergers and credit risk are related, according to numerous studies by Knapp and Gart (2014) and Bonaccorsi di Patti and Gobbi (2003). The work of Weiß et al. (2014) has been crucial in the development of numerous systemic risk dimensions. Acharya et al. (2012) examine a novel methodology for assessing and overseeing systemic risks in the event of a deficit in capital. Billio et al. (2012) discussed econometric measures to assess connectedness and systemic risk within the finance and insurance sector. These discoveries have extensive implications for future academics and researchers, as M&A in the banking sector could promote interdisciplinary research. Academics from various fields, such as finance, economics, law, and management, can collaborate to investigate the complex issues related to M&A deals in the banking sector (Jallad et al., 2025). Connecting the numerous subfields identified in this study could aid them in evaluating the quality of ‘bank merger research’ and provide them with anticipated new avenues to pursue.

The stated objective has the potential to generate novel insights within the domain of bank mergers, a field that is undergoing continuous evolution and is marked by the contributions of numerous researchers. This study is likely to be useful to both doctoral students (who seek a general comprehension of ‘bank mergers’ to guide their work) and seasoned academics (who seek out active research opportunities and publish authoritative literature opinions).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Acemoglu, D., Ozdaglar, A., & Tahbaz-Salehi, A. (2015). Systemic risk and stability in financial networks. American Economic Review, 105(2), 564–608.

Acharya, V. V., Bharath, S. T., & Srinivasan, A. (2007). Does industry-wide distress affect defaulted firms? Evidence from creditor recoveries. Journal of Financial Economics, 85(3), 787–821.

Acharya, V. V., Engle, R., & Richardson, M. (2012). Capital shortfall: A new approach to ranking and regulating systemic risks. American Economic Review, 102(3), 59–64.

Acharya, V. V., Pedersen, L. H., Philippon, T., & Richardson, M. (2017). Measuring systemic risk. Review of Financial Studies, 30(1), 2–47.

Allen, F., & Gale, D. (2004). Competition and financial stability. Journal of Money, Credit and Banking, 36(3), 453–480.

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 23(4), 589–609.

Altman, E. I. (2018). A fifty-year retrospective on credit risk models, the Altman Z-score family of models and their applications to financial markets and managerial strategies. Journal of Credit Risk, 14(4), 1–34.

Asandului, M., Cazan, S. A., Capraru, B., & Ihnatov, I. (2016). The impact of bank mergers and acquisitions on the bank performance and risk taking behaviour. Transformations in Business & Economics, 15.

Baker, H. K., Kumar, S., & Pandey, N. (2020). A bibliometric analysis of European Financial Management’s first 25 years. European Financial Management, 26(5), 1224–1260.

Baker, H. K., Kumar, S., & Pattnaik, D. (2020). Fifty years of The Financial Review: A bibliometric overview. Financial Review, 55(1), 7–24.

Battiston, S., D’Errico, M., & Gurciullo, S. (2016). DebtRank and the network of leverage. Journal of Private Equity, 20(1), 58–71.

Bellovary, J. L., Giacomino, D. E., & Akers, M. D. (2007). A review of bankruptcy prediction studies: 1930 to present. Journal of Financial Education, 33, 1–42.

Berger, A. N. (2018). The benefits and costs of the TARP bailouts: A critical assessment. Quarterly Journal of Finance, 8(02), 1850011.

Billio, M., Getmansky, M., Lo, A. W., & Pelizzon, L. (2012). Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics, 104(3), 535–559.

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637–654.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

Bojovi.png) , S., Mati, R., Popovi, Z., Smiljani, M., Stefanovi, M., & Vidakovi, V. (2014). An overview of forestry journals in the period 2006–2010 as basis for ascertaining research trends. Scientometrics, 98(2), 1331–1346. https://doi.org/10.1007/s11192-013-1171-9

, S., Mati, R., Popovi, Z., Smiljani, M., Stefanovi, M., & Vidakovi, V. (2014). An overview of forestry journals in the period 2006–2010 as basis for ascertaining research trends. Scientometrics, 98(2), 1331–1346. https://doi.org/10.1007/s11192-013-1171-9

Bonaccorsi di Patti, E., & Gobbi, G. (2003). The effects of bank mergers on credit availability: Evidence from corporate data (No. 479). Bank of Italy, Economic Research and International Relations Area.

Botelho, L. L. R., Cunha, C. C. D. A., & Macedo, M. (2011). O método da revisão integrativa nos estudos organizacionais. Gestão e Sociedade, 5(11), 121–136.

Bourdieu, P. (1994). O campo científico. In R. Ortiz (Ed.), Pierre Bourdieu: Sociologia (2nd ed., pp. 122–155). Ática.

Brealey, R. A., Cooper, I. A., & Kaplanis, E. (2019). The effect of mergers on US bank risk in the short run and in the long run. Journal of Banking & Finance, 108, 105660.

Brunnermeier, M. K., & Cheridito, P. (2019). Measuring and allocating systemic risk. Risks, 7(2), 46.

Burnham, J. F. (2006). Scopus database: A review. Biomedical Digital Libraries, 3(1), 1.

Chiaramonte, L., Dreassi, A., Piserà, S., & Khan, A. (2023). Mergers and acquisitions in the financial industry: A bibliometric review and future research directions. Research in International Business and Finance, 64, 101837.

De Bandt, O., & Hartmann, P. (2000). Systemic risk: A survey. SSRN. https://doi.org/10.2139/ssrn.258430

de Moya-Anegón, F., Chinchilla-Rodríguez, Z., Vargas-Quesada, B., Corera-Álvarez, E., Muñoz-Fernández, F. J., González-Molina, A., & Herrero-Solana, V. (2007). Coverage analysis of Scopus: A journal metric approach. Scientometrics, 73(1), 53–78.

Dube, S., & Glascock, J. L. (2006). Effects of the method of payment and the mode of acquisition on performance and risk metrics. International Journal of Managerial Finance, 2(3), 176–195.

Duffie, D. (2005). Credit risk modeling with affine processes. Journal of Banking & Finance, 29(11), 2751–2802.

Duffie, D., & Lando, D. (2001). Term structures of credit spreads with incomplete accounting information. Econometrica, 69(3), 633–664.

Eisenberg, L., & Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2), 236–249.

Feito-Ruiz, I., & Menéndez-Requejo, S. (2013). Acquisition of listed vs unlisted firms: Determinants in different legal and institutional environments. SSRN. https://doi.org/10.2139/ssrn.2291049

Ferreira, M. P., Santos, J. C., de Almeida, M. I. R., & Reis, N. R. (2014). Mergers and acquisitions research: A bibliometric study of top strategy and international business journals, 1980–2010. Journal of Business Research, 67(12), 2550–2558.

Goodell, J. W., Kumar, S., Lim, W. M., & Pattnaik, D. (2021). Artificial intelligence and machine learning in finance: Identifying foundations, themes, and research clusters from bibliometric analysis. Journal of Behavioral and Experimental Finance, 32, 100577.

Goyal, K. A., & Joshi, V. (2011). Mergers in banking industry of India: Some emerging issues. Asian Journal of Business and Management Sciences, 1(2), 157–165.

Hassan, M., & Giouvris, E. (2021). Bank mergers: The cyclical behaviour of regulation, risk and returns. Journal of Financial Economic Policy, 13(2), 256–284.

Homburg, C., & Bucerius, M. (2005). A marketing perspective on mergers and acquisitions: How marketing integration affects postmerger performance. Journal of Marketing, 69(1), 95–113.

Jallad, R. F., Tina, A., & Persakis, A. (2025). Mergers and acquisitions’ moderating effect on the relationship between credit risk and bank value: A quantile regression approach. Journal of Risk and Financial Management, 18(2), 100.

Khan, A., Hassan, M. K., Paltrinieri, A., Dreassi, A., & Bahoo, S. (2020). A bibliometric review of takaful literature. International Review of Economics & Finance, 69, 389–405.

Knapp, M., & Gart, A. (2014). Post-merger changes in bank credit risk: 1991–2006. Managerial Finance, 40(1), 51–71.

Kress, J. C. (2020). Modernizing bank merger review. Yale Journal on Regulation, 37, 435.

Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275.

Laeven, L., & Valencia, F. (2013). Systemic banking crises database. IMF Economic Review, 61(2), 225–270.

Liu, W., Gu, M., Hu, G., Li, C., Liao, H., Tang, L., & Shapira, P. (2014). Profile of developments in biomass-based bioenergy research: A 20-year perspective. Scientometrics, 99(2), 507–521. https://doi.org/10.1007/s11192-013-1152-z

Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance, 29(2), 449–470.

Merton, R. C., & Thakor, R. T. (2019). Customers and investors: A framework for understanding the evolution of financial institutions. Journal of Financial Intermediation, 39, 4–18.

Moher, D., Liberati, A., Tetzlaff, J., Altman, D. G., & Prisma Group. (2010). Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. International Journal of Surgery, 8(5), 336–341.

Molyneux, P., Schaeck, K., & Zhou, T. M. (2014). Too systemically important to fail in banking: Evidence from bank mergers and acquisitions. Journal of International Money and Finance, 49, 258–282.

Moschieri, C., & Campa, J. M. (2014). New trends in mergers and acquisitions: Idiosyncrasies of the European market. Journal of Business Research, 67(7), 1478–1485.

Ngo, H. (2019). The effects of mergers and acquisitions on bank risks (Doctoral dissertation, University of Westminster).

Nguyen, P., Ben Zaied, Y., & Pham, T. P. (2019). Does idiosyncratic risk matter? Evidence from mergers and acquisitions. Journal of Risk Finance, 20(4), 313–329.

Paltrinieri, A., Hassan, M. K., Bahoo, S., & Khan, A. (2023). A bibliometric review of sukuk literature. International Review of Economics & Finance, 86, 897–918.

Papadakis, V. M., & Thanos, I. C. (2010). Measuring the performance of acquisitions: An empirical investigation using multiple criteria. British Journal of Management, 21(4), 859–873.

Patel, R., Goodell, J. W., Oriani, M. E., Paltrinieri, A., & Yarovaya, L. (2022). A bibliometric review of financial market integration literature. International Review of Financial Analysis, 80, 102035.

Paul, J., & Dhiman, R. (2021). Three decades of export competitiveness literature: Systematic review, synthesis and future research agenda. International Marketing Review, 38(5), 1082–1111.

Price, D. J. de S. (1965). Networks of scientific papers: The pattern of bibliographic references indicates the nature of the scientific research front. Science, 149(3683), 510–515.

Reddy, K. S., Yadav, R. S., & Agarwal, A. (2025). Credit exposures and systemic risk in Indian banks. Asian Journal of Economics and Banking, 9(2), 222–239.

Salas, V., & Saurina, J. (2003). Deregulation, market power and risk behaviour in Spanish banks. European Economic Review, 47(6), 1061–1075.

Saunders, A., & Walter, I. (2012). Financial architecture, systemic risk, and universal banking. Financial Markets and Portfolio Management, 26, 39–59.

Schoenberg, R. (2006). Measuring the performance of corporate acquisitions: An empirical comparison of alternative metrics. British Journal of Management, 17(4), 361–370.

Sharifi, S., Haldar, A., & Rao, S. N. (2019). The relationship between credit risk management and non-performing assets of commercial banks in India. Managerial Finance, 45(3), 399–412.

Soedarmono, W., Sitorus, D., & Tarazi, A. (2017). Abnormal loan growth, credit information sharing and systemic risk in Asian banks. Research in International Business and Finance, 42, 1208–1218.

Thorbjørnsen, H., & Dahlén, M. (2011). Customer reactions to acquirer-dominant mergers and acquisitions. International Journal of Research in Marketing, 28(4), 332–341.

Van Dellen, S., Benamraoui, A., Ngo, H., & Salaber, J. (2018). The effects of mergers and acquisitions on acquiring banks’ contribution to systemic risk. In 11th international risk management conference (Risk society).

Van Eck, N. J., & Waltman, L. (2010). Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics, 84(2), 523–538.

Weber, Y., Tarba, S. Y., & Öberg, C. (2014). A comprehensive guide to mergers and acquisitions: Managing the critical success factors across every stage of the M&A process. Pearson & Financial Times Press.

Weiß, G. N., Neumann, S., & Bostandzic, D. (2014). Systemic risk and bank consolidation: International evidence. Journal of Banking & Finance, 40, 165–181.

Zupic I., & .png) ater T. (2015). Bibliometric methods in management and organization. Organizational Research Methods, 18(3), 429–472.

ater T. (2015). Bibliometric methods in management and organization. Organizational Research Methods, 18(3), 429–472.